Five years ago, carbon removal technology would have been uttered in the same breath as pie-in-sky climate solutions such as solar geo-engineering – i.e. artificially dimming the sun. Today, the scientific community sees carbon removal markets as necessary and scalable. They will be key to the world’s ambition of limiting global warming to a just-about-manageable 1.5°C. According to the Intergovernmental Panel on Climate Change’s (IPCC) latest report, “reaching net zero GHG emissions primarily requires deep reductions in CO₂, methane, and other GHG emissions, and implies net-negative CO₂ emissions. Carbon dioxide removal will be necessary to achieve net-negative CO₂ emissions”.

Carbon removal, or carbon dioxide (CO₂) removal (CDR), encompasses both natural solutions such as sequestering and storing carbon in trees and soil, and technology that extracts CO₂ directly from the atmosphere. Exactly how much CO₂ will need to be removed depends on how rapidly and by how much emissions can be reduced across sectors, but the IPCC estimates that by 2050, an eye-watering 5–16 gigatonnes (Gt) of CO₂ will have to be extracted annually across the planet.

Go deeper with GlobalData

That grand ambition took one step closer to reality over the past two months as a litany of landmark deals announced the arrival of CDR as a commercial market finally able to stand on its own two feet.

“The CDR market is taking off,” says Rudy Kahsar, manager of the CDR team at the US-based think tank RMI. “CDR is becoming less controversial; it is in a sweet spot of expansion without any major failures. Demand signals are very strong from both the public and private sectors, and supply is picking up momentum. Buyers are also becoming wary of low-quality offsets – this is pushing for better rules, which will push more voluntary money into CDR.”

Big deals

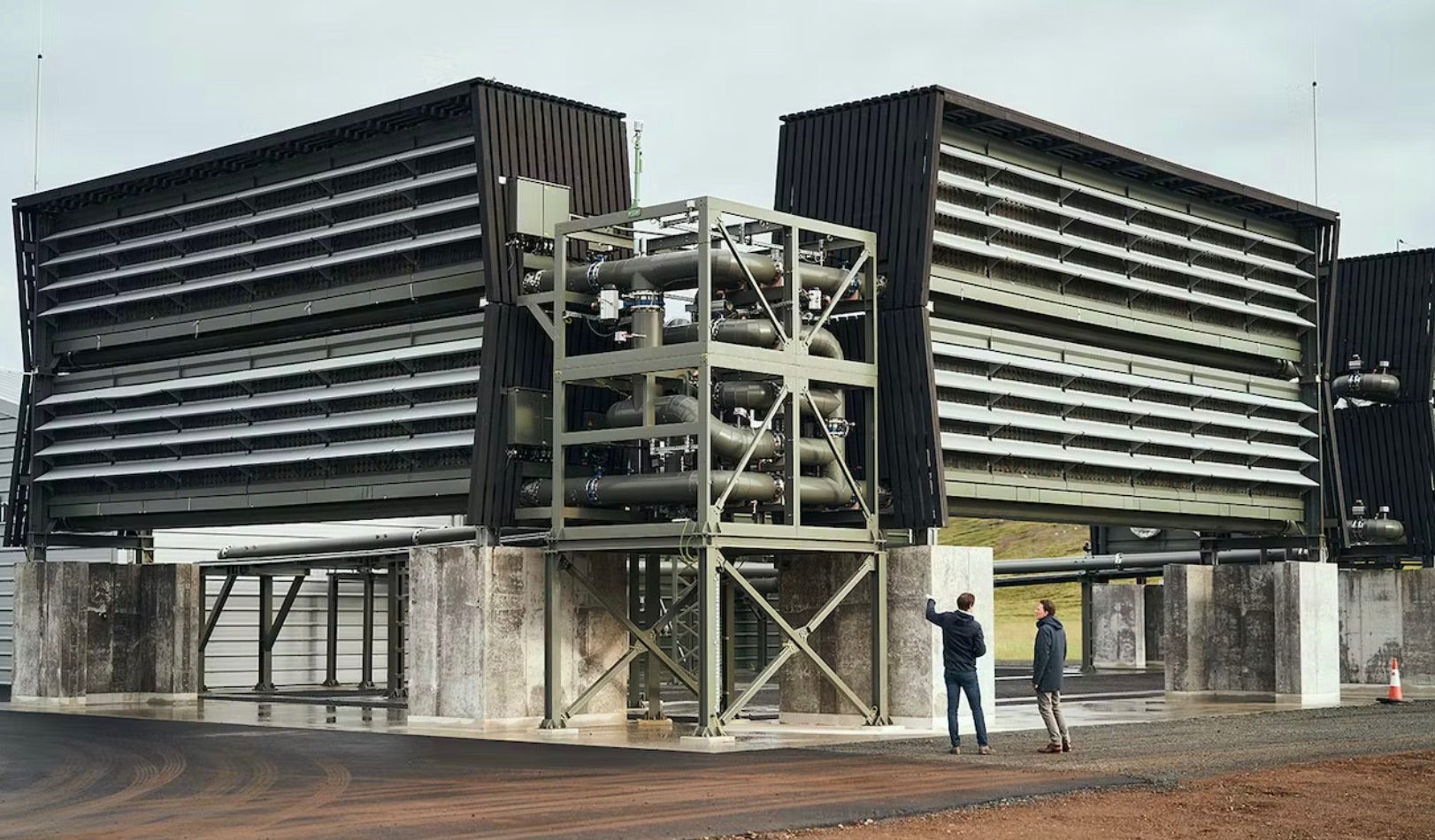

On 23 May, banking giant JPMorgan Chase announced it had signed long-term agreements to purchase more than $200m of CDR. The agreements, intended to remove and store 800,000 tonnes of carbon dioxide equivalent (tCO₂e) from the atmosphere, represented one of the largest carbon removal purchases announced to date.

These included a nine-year agreement with Climeworks to deliver 25,000tCO₂e of carbon removal services via direct air capture and storage (DACS); a five-year deal to purchase Charm Industrial’s bio-oil CDR, removing and storing approximately 28,500tCO₂e (deliveries have already begun for JPMorgan Chase); a memorandum of understanding (MoU) with CO280 Solutions reflecting the bank’s intent to purchase up to 30,000tCO₂e of CDR per year for delivery over up to 15 years, for an expected total removal of as much as 450,000tCO₂e; and a $75m commitment to Frontier, a Stripe-managed advance market commitment aimed at accelerating carbon removal by guaranteeing demand, which saw the bank commit $50m to CDR credits for its own operational emissions and $25m for credits to help clients meet their climate targets.

Just a week earlier, Microsoft had agreed to purchase a whopping 2.76 million tonnes of carbon removal over 11 years from Ørsted’s Asnæs Power Station – officially the world’s largest carbon removal offtake agreement by volume. The project involves installing carbon capture technology at Ørsted’s wood chip-fired Asnæs Power Station in the Danish city of Kalundborg in western Zealand. The combined heat and power plant will start to capture and store biogenic carbon in 2025 and will capture and store around 430,000t of biogenic CO₂ every year from the start of 2026.

Around the same time, Charm Industrial disclosed a $53m multi-year contract with Frontier. Under the agreement, the San Francisco-based company will remove 112,000t of CO₂ from the atmosphere between 2024 and 2030 on behalf of the corporations behind Frontier. Charm Industrial’s approach converts waste biomass from agricultural harvests and forest fire management to a bio-oil, which is then injected into storage wells underground, durably storing the CO₂ that otherwise would have been released during decomposition.

At the end of April, NextGen CDR Facility (NextGen), a joint venture between Swiss carbon finance consultancy South Pole and Japanese conglomerate Mitsubishi Corporation, announced the advance purchase of 193,125t of CDRs to create the world’s largest diversified portfolio of CDR projects, offering more than 1,000 years of CO₂ storage once delivered. The advance purchase will include CDRs from the world’s largest DACS project, being developed by 1PointFive in Texas, which is expected to remove and permanently store up to 500,000t of CO₂ per year once fully operational. There will also be CDRs from the world’s largest tech carbon removal project, the Summit Carbon Solutions $5.1bn biomass carbon removal and storage project under development in the US Midwest, which will remove more than nine million tonnes annually via the capture, transportation and permanent storage of biogenic carbon removals. In addition, the portfolio will acquire carbon removal credits from climate tech company Carbo Culture’s inaugural high-technology biochar project in Finland, with the first series of commercial facilities due to produce biochar to remove and durably store 2.5 million tonnes of CDRs by 2030.

Keep up with Energy Monitor: Subscribe to our weekly newsletterThere were a few other important deals that flew under the radar during the PR pyrotechnics of the above mega agreements. On 31 May, Equatic, a University of California, Los Angeles, spin-out pairing CO₂ removal using seawater and hydrogen production, unveiled a major deal with Boeing. Under the pre-purchase agreement, over a five-year period starting mid-decade, Equatic will remove 62,000t of CO₂ and deliver 2,100t of carbon-negative hydrogen to Boeing.

On 11 May, UK-based power generator Drax agreed an MoU with C-Zero Markets in relation to the sale of CO₂ removal credits from Drax’s first US bioenergy with carbon capture and storage facility. Under the terms of the MoU, Drax and C-Zero will work together with a view to C-Zero acquiring 2,000t of CDRs for $300 per tonne (/t).

In March, ocean health company Running Tide announced an agreement with Microsoft for ocean-based CO₂ removal, using technology that accelerates the ocean’s ability to naturally remove CO₂ and permanently sink it to the deep ocean. Under the agreement, Running Tide will remove 12,000tCO₂e on behalf of Microsoft.

Carbon removal markets: 300% growth in two months

All these recent deals have lit a fire under the CDR market. Since April, the market has grown by close to 300%, from just over one million tonnes of purchased CO₂ to close to four million tonnes today, according to carbon removal analytics website CDR.fyi. Ørsted, Drax and CO280 top the charts for the most tonnes sold with 2.7 million, two million and 450,000 tonnes, respectively.

To caveat all that, only 1.9% of those purchases have been delivered so far. However, that is to be expected because of the long-term nature of the contracts, the nascent state of the technology and the rapid recent growth of the market from its low base. Deliveries, nevertheless, have still been rising at a fast pace: from just 136t in June 2019 to more than 74,000t today. Three companies specialising in biochar – created via pyrolysis of residual biomass and subsequently stored long-term in soils or durable materials such as cement and tar – have delivered the most CDRs to date: Wakefield Biochar (20,000t), Douglas County Forest Products (11,000t) and Freres Biochar (6,000t).

In terms of hard cash, this fast take-up has seen the value of the market go from entirely worthless in January 2020 to close to $400m today. Microsoft has been by far the largest investor in the space, buying 2.82 million tonnes of CDRs to date, followed by Airbus at 400,000t and NextGen at 193,000t.

“There is a splitting happening in the carbon markets,” explains Kahsar. “Forward-thinking organisations are increasingly passing on traditional forest-based carbon avoidance projects – which people are starting to realise are low-quality and short-term – in favour of permanent carbon removals. There is a growing realisation that preventing someone from cutting down a forest for ten years is just not going to cut it; and the likes of Frontier, Microsoft and the airlines are now exclusively focusing on removals.”

The momentum behind carbon removal markets, Kahsar recollects, started with the IPCC’s famous “1.5°C report” back in 2018, which first introduced a target for carbon removals. That was then expanded on in the IPCC’s 2022 edition. Since then, the US’s Inflation Reduction Act, which increased the 45Q tax credit to $180/t for direct air capture injection, has provided further impetus for investment in the space.

“Things have all sort of come together and climate-aligned companies are now competing to lead on CDR, which is why we are seeing all these announcements about deployments,” says Kahsar. “There is going to be even more to come in the next year or two.”

A drop in the ocean

However, before anyone gets too carried away, there is a long way to go before the carbon removals market reaches the IPCC’s desired target of circa 10Gt a year by 2050. For visual reference, that would mean the market has to grow from 74,000t of captured CO₂ in total today to 10,000,000,000 tonnes every year by 2050. It will be a monumental undertaking.

“In our technology-oriented world, we are used to seeing things increase in capacity exponentially year after year, such as the processing power of computer chips,” says Antti Vihavainen, CEO of carbon removal platform Puro.earth “But a gigatonne of carbon is huge – saying a gigatonne is easy, but we first have to fight our way to a megatonne, and then make that a thousand times over. So, to get there, we have to grow at an incredible pace – today and for many, many years. But innovation happens when there is demand and we shouldn’t think anything is impossible.”

Impossible, no, but the task may have become even more Herculean after, at the end of May, the UN Framework Convention on Climate Change (UNFCCC), an influential climate panel tasked with guiding the creation of a new global carbon market, sent shockwaves through the industry by casting doubt on whether CDR would be counted as a carbon offset.

Read more from this author: Oliver GordonThe guidance included a technical note stating that "engineered carbon removal activities... do not contribute to sustainable development", and fail to serve the goals of the carbon market under the Paris Agreement. The note came from the Article 6.4 Supervisory Body, part of the UN climate bureaucracy spearheading the future of global carbon markets. The proposal, which has not been approved, also calls carbon removal solutions "technologically and economically unproven, especially at scale", and says the technology poses "unknown environmental and social risks". More than 100 companies and organisations have since signed a letter to the UNFCCC’s secretariat objecting to the draft guidance.

In truth, climate purists have always baulked at CDR, believing it a distraction from the fundamental task of decarbonising the global economy. Nonetheless, even if the UNFCCC’s position stays the same – which seems unlikely – there is, realistically, no putting the genie back in the bottle now. The world has already reached 1.1°C of the 1.5°C global warming target it is trying to avoid, and global emissions are still rising. Governments and companies are lagging behind in the race to net-zero emissions by 2050 and will need all the help they can get – so much so, in fact, that people are now seriously considering geo-engineering approaches such as brightening the clouds, which would have made Isaac Asimov chuckle. Consequently, it is hard to imagine the meteoric growth of the carbon removals market as anything but inexorable.

“It is important that carbon offsets don’t become an excuse for companies not to decarbonise,” says Callum Hunt, a carbon specialist at carbon offset procurement platform Abatable. “But we will need CDR for the hard-to-abate emissions, so we need to scale the market right now for it to be ready in time. There are some industries – like aviation, steel and cement – that won’t be able to decarbonise in time for 2050, so the CDR industry will need to be ready to fill the gap.”