Demand forecasts converge in 2025. China and non-Organisation for Economic Co-operation and Development (OECD) growth, Europe transition, and US shift to watch. Majors consolidate but spread long-term risk by planting seeds in renewable technology. President Trump will be the largest source of disruption in 2025, with policy realignment vis-à-vis allies, trading partners, and foes.

The year 2024 saw significant developments in the oil and gas (O&G) space. Oil demand shifts, diversifying and growing portfolios, technology breakthroughs, and major geopolitical events of 2024 will continue to play out in 2025, with significant disruptive impact from the new Trump presidency. This O&G Research Insights edition from leading data and analytics company GlobalData will outline the key trends as an outlook for 2025:

Global demand shifts

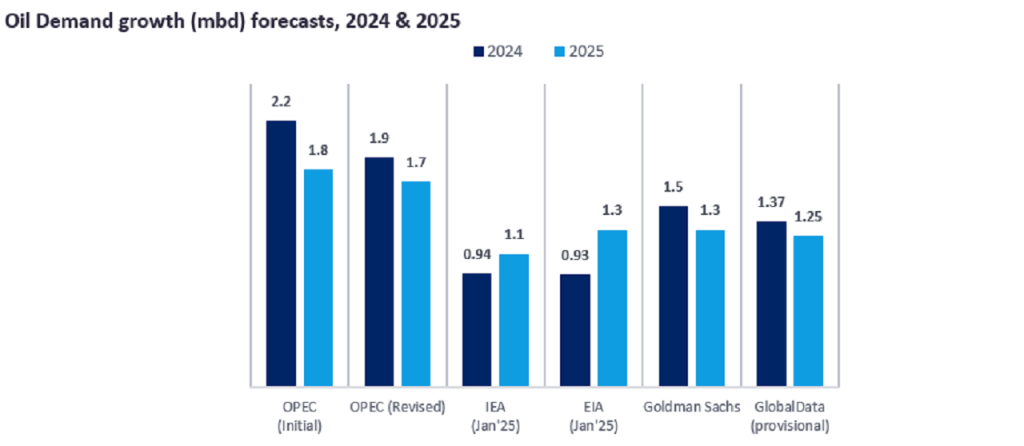

Global demand for oil defied bullish expectation of the Organization of the Petroleum Exporting Countries (OPEC), repeatedly putting out downward revisions, and the more bearish International Energy Agency forecasts. Europe seemingly peaked its gas demand, three years after the start of the Russia-Ukraine conflict.

The US, and North America as a whole, has not peaked yet and saw modest growth. Trump’s election and ongoing bills in Congress (EPRA; HR1, LECA) will delay that peak further by lowering the relative cost and ease of fossil-fuel projects. China’s economic woes have been the primary cause for constant downward revisions of global oil demand forecasts by OPEC, making India the largest driver of oil and gas demand globally. The impact of adoption of electric vehicles and renewables remains hard to predict, with overshoots in 2022 and undershoots in 2024. Their impact on future primary energy demand in non-OECD countries will determine future oil and gas demand.

Forecasts in 2024 diverged widely, after different calibrations of the post-Covid bounce, adoption of renewables, and Chinese growth expectations. On the other hand, 2025 will see most forecasts converge in the mid-to-low one million barrels per day of global demand growth. Gas, being steadily used as a transition fuel and displacing coal in power generation, will see continued demand growth.

Greener portfolios

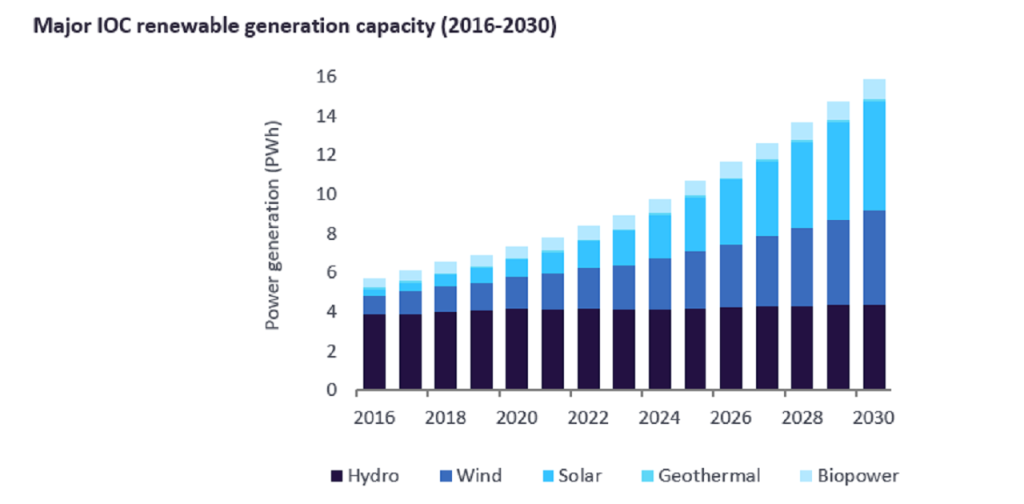

Major O&G companies have increasingly diversified portfolios, either downwards into refining and petrochemicals, or into renewable energy, with upstream-associated or stand-alone green projects. Investment in renewables serves a dual purpose: Diversify and plant the seeds for a futureproof portfolio, and – depending on local regulations – use them for carbon credits, used as offsets in compliance and voluntary carbon markets. Leaders include TotalEnergies, Shell, BP, Equinor, and Petrobras.

How well do you really know your competitors?

Access the most comprehensive Company Profiles on the market, powered by GlobalData. Save hours of research. Gain competitive edge.

Thank you!

Your download email will arrive shortly

Not ready to buy yet? Download a free sample

We are confident about the unique quality of our Company Profiles. However, we want you to make the most beneficial decision for your business, so we offer a free sample that you can download by submitting the below form

By GlobalData

Consolidation

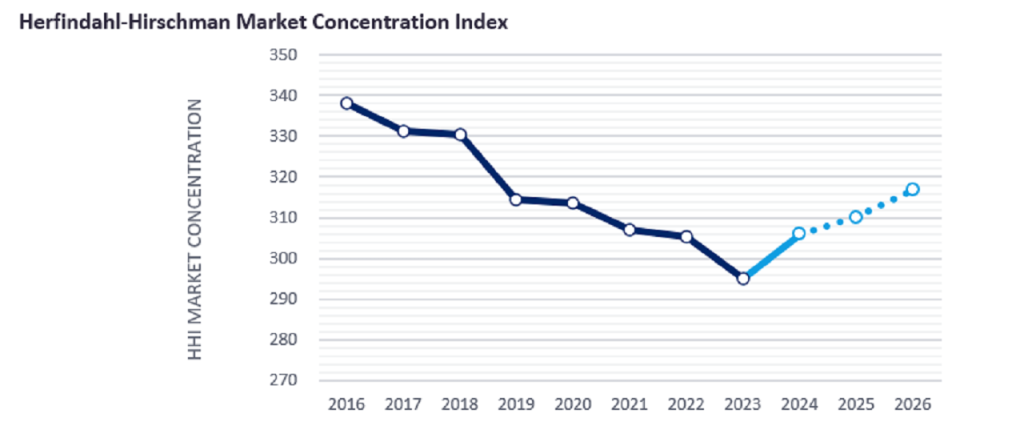

Moreover, there is a trend for consolidation, with O&G majors increasing market cap through large merger and acquisition deals. These include the acquisitions of Marathon Oil, Pioneer, and Hess. The Herfindahl-Hirschman Index shows increased upstream competition since 2016, but, according to GlobalData’s Field Database, 2024 marked the start of visible consolidation in production share, expected to continue in 2025, with current development plans and loosened US regulation.

Geopolitical tensions

Turbulence is the oil and gas market’s bread and butter, and 2024 saw prolonged and renewed tensions arising, which shaped peaks and lows in oil and gas prices. Significant oil growth in non-OPEC and the Americas, amidst a decelerating oil demand, has seen prices largely weaken, despite OPEC cutting oil supply four times since 2022. Subsequently, the release of withheld production has been delayed four times since August 2024. Developments around the strait of Hormuz, seeing 20% of global oil trade pass through, and the fate of sanctions on Russia will be on the main stage throughout 2025.

Trump 2.0 will be the largest source of disruption in 2025. Tensions with key allies such as Canada, Mexico, and Europe, rivals and partners such as China, and foes, Iran, Russia and Venezuela, will have effects on the oil and gas markets.

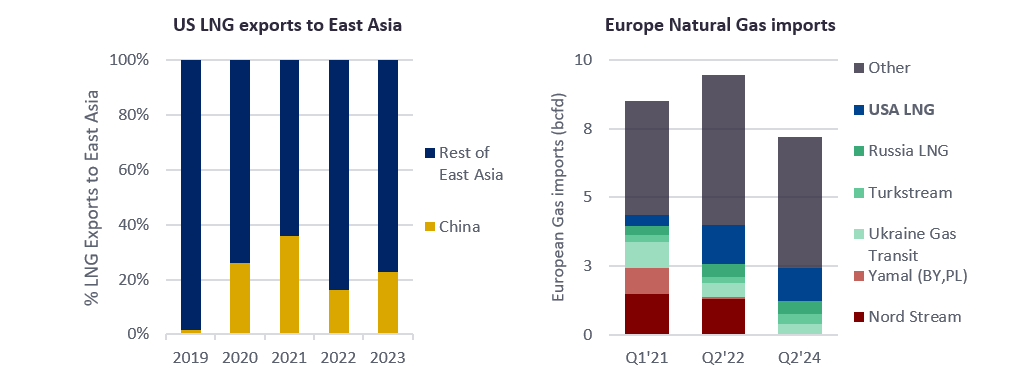

Growing US-Canada tension has seen Canadian officials threaten to cut energy exports to the US. Furthermore, with roughly 100 million tonnes per annum in liquified natural gas (LNG) export capacity growth by 2030, Mexico and Canada will look to rival the US’ current trading partners, though not truly until 2027. A major surge in the whole of NA’s LNG export capacity will put pressure on domestic gas markets.

Biden used LNG exports as a tool to strengthen ties with key allies. Trump is more likely to use it as leverage in negotiating trade agreements and financing joint organisations. European countries may find themselves under increased pressure to reduce overall gas demand, turning to renewables at a quicker pace.

Technology adoption

Increased AI adoption improved predictive maintenance, helped to optimise production processes, and facilitated data-driven strategies, leading to cost reductions and increased productivity. Adoption will remain concentrated in higher-income countries, which also have higher regulatory pressures for energy efficiency and emissions mitigation. These pressures will take oil and gas operations towards electrification and adoption of carbon capture, utilisation and storage and other emissions reduction technologies. Tech disruption and capital market expectations in the US will push tech adoption, despite less regulatory pressure.

Bottom line

Oil and gas markets will face a pivotal landscape in 2025, shaped by converging fossil-fuel demand, geopolitical shifts, and greener and wider portfolios. Explore GlobalData’s Oil and Gas Intelligence Center to access the data and insights your organisation needs to navigate 2025.

Related Company Profiles

TotalEnergies SE

Shell plc

BP Plc

Equinor ASA

Marathon Oil Corp